National Economic Recovery Plan (PENJANA): Taking advantage of the property market

A welcome respite for the property market

On June 5 2020, Prime Minister Tan Sri Muhyiddin Yasin announced the inception of the National Economic Recovery Plan, or PENJANA to help revitalize Malaysia’s economy following the wake of Covid-19 and MCO 2020, which severely hampered the country’s economic well being.

The plan, which targets some of Malaysia’s key economic sectors, aims to provide attractive financial assistance to many individuals and enterprises affected by the pandemic, namely the B40s and SMEs. In layman terms, the government hopes to encourage spending amongst consumers, which creates market robustness and thereby stabilizing the country’s ailing economy, if not improving it. Some keyeconomic sectors listed within PENJANA include but are not limited to:

The tourism industry

Education sectors

Financial sectors

Art, Culture & Entertainment sectors

National healthcare

And most importantly, the property sector.

For the property sector, this is manifested through the introduction ofHome Ownership Campaign 2021, commonly known as HOC 2021.

The backstory of HOC

Back in 2019, the country saw a total of 40916 residential units left unsold and unoccupied, causing the government to rake in a loss of RM27.38 billion that year. This spurred the Ministry of Housing and Local Government (KPKT) to collaborate withREHDA 和MIEA to conceive HOC, an initiative that provides Malaysians with various financial incentives in homebuying in hopes of encouraging property spending.

HOC 2019 performance

HOC 2019 was well-received by many property developers during its unveiling and saw as many as 51 developer names joining the organizations’ efforts to curb property overhang.

Overall, the initiative saw marginal success, allowing the government torecoup a loss amounting to RM12.5 billion total, almost 50% recovery. In fact, HOC 2019 was so well received that the government extended its run by another six months, from 1 Jan 2019 – 30 June 2019, to 1 Jan 2019 – 31 Dec 2019. This allowed the government to continue recouping further financial losses from property overhang, whilst still enabling further interested parties to come forward and spend.

Although the government saw great success in curbing property overhang, the battle to eliminate the problem was far from over. Unfortunately, just as things were starting to look up for the property market, the Covid-19 pandemic came and worsened things.

A comeback

It should come as no surprise that property developers are one of the business entities affected throughout MCO. Ditto property buyers too. Essentially, no one was spared from the wrath of Covid-19.

In spite of the clear mismatch in rising demands from fellow Malaysians for houses and property supply from the market for anumber of reasons, developers continued churning out houses ever so often.

Alas, this has aggravated the issue of property overhang all over again, and reset any property overhang-curbing efforts back to square one. Additionally, the government is presented with a new issue, a badly hit economy.

Subsequently, this led the government to reintroduce HOC into the fray as a part of PENJANA. Named HOC 2021, the initiative returns with all the benefits and incentives provided by its 2019 predecessor. This time however, HOC 2021’s first and foremost role is to reinvigorate the country’s economy, while its property overhang crusading efforts take the backseat.

HOC 2021’s perks

Set to run from 1 June 2020 – 31 Dec 2021, HOC 2021 provides the following benefits to entice Malaysians to spend on properties.

10% discount on property price

The first benefit of HOC is the 10% discount that it provides to fellow homebuyers. To qualify for this promotional discount, you must first ensure that the developer is registered under REHDA, SHEDA or SHAREDA, or else your purchased property will not qualify for the benefit.

The process for the 10% discount is straightforward. Upon purchasing your property, a 10% discount applies. Assuming you have made a down payment, the discount will apply to the remaining price instead.

Stamp duty waiver

Buying a house involves more than just forking out the down payment and paying the home alone. In fact, there are a slew of additional costs that come with it, like stamp duties. Stamp duties are basically legal documents to officiate and formalize the transfer of an asset from one party to another, i.e., Properties. In this context, it is the transfer of ownership from the developer to the buyer aka the soon-to-be owner.

Stamp duties are important for many reasons, but the two biggest ones are proof of ownership of property, and it serves as a form of legal evidence in court where property disputes are concerned.

While homebuyers can technically apply for stamp duties via Malaysia’s e-stamp duty, Lembaga Hasil Dalam Negeri (LHDN), most prefer to have it vetted and handled by legal practitioners who are well-versed with laws concerning properties and lands. Since homebuyers will be consulting a professional to take care of the hassle, they are expected to pay a fee.

Two main forms of stamp duties are involved in the transferral of ownership:

Instrument of Transfer & Loan Agreement

买卖协议(SPA)

Stamp duties usually set you back by RM1000 – RM2000 on average. Though under PENJANA: HOC 2021, the costs are done away.

70% credit limit uplift for third properties

Banks approve your request for a housing loan based on your debt-service ratio (DSR), which is determined through this formula.

Debt/Net Income * 100

A rule of thumb is to keep your DSR within the range of 60 – 75%, as that is the sweet spot for banks to grant you a housing loan. Failure to do so results in banks denying your request for one, or granting a loan that is substantially lower.

Typically, most individuals receive a 90% housing loan when buying their first and second property. On their third property onwards however, they only receive 70% housing loan from banks.

Thankfully, in conjunction with HOC 2021, the government has lifted the 70% credit limit, which means people purchasing their third property can now enjoy a 90% housing loan too.

Regardless of a 70% or 90% housing loan, it’s important to remember that several other factors also determine your eligibility for one, like credit scores and the loan-to-value ratio. So it would be wise for you to keep tabs on these before applying for a loan.

Removal of RPGT

Real Property Gains Tax, or RPGT is a tax that applies to individuals who have successfully sold off their property aka subsale property. For every subsale property sold, the government taxes sellers at a rate between 5 – 30%, depending on the age of their home and the profit made.

Under the effects of HOC 2021, the RPGT is exempted, and the benefit extends to two more properties per seller, meaning they can sell a total of three subsale properties without being taxed.

Essentially, citizens who are experiencing any financial woes as a result of the pandemic can liquidate their property by selling them with no additional costs involved.

In a nutshell, the goal of HOC 2021 is to encourage Malaysians to spend and invest in properties. By eliminating some of the additional costs involved, the government hopes to incentivize all property players to come forward and spend or sell their property. One way or the other, this generates revenue for the government and ultimately keeps the country’s economy afloat.

Reception

Responses towards HOC 2021 are generallypositive, with many experts claiming that the initiative will increase the property market’s appeal to the public, and coax consumers to “at least consider the idea of buying a home during MCO.”

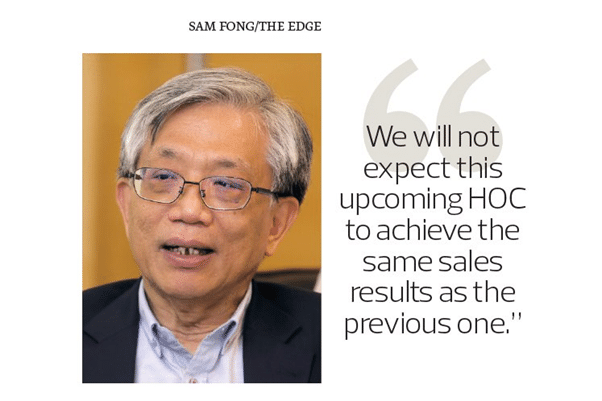

That said, given the circumstances that the country had and still has, many remain cautiously optimistic about the property market’s outlook, and predict HOC 2021 to have a lesser presence than its 2019 counterpart. In fact, a few have even spoken out against the plan.

In particular, CEO of Henry Butcher (M) Sdn Bhd, Tang Chee Meng believes that despite the financial incentives provided by the government, the pandemic will deter people from purchasing big-ticket items. Additionally, he stated that banks are more likely to be wary of the discounts and rebates offered by developers and as such, will offer loans with lesser value to err on the side of caution.

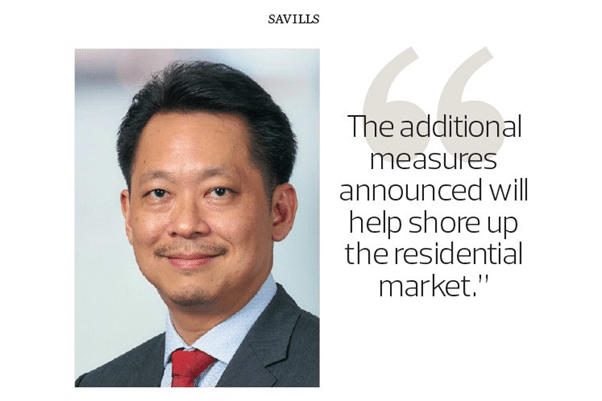

Meanwhile, Savills (M) Sdn Bhd managing director, Datuk Paul Khong expressed his disappointment towards PENJANA, claiming that while the initiative would trim off some of the challenges posed by the pandemic, there was a clear lack of attention being put forth into the planning of HOC 2021 as far as the wellbeing of the property market is concerned.

Tang Chee Meng and Datuk Paul Khong pictured above, both who were critical about PENJANA. Picture courtesy of TheEdgeMarkets

Nonetheless, like the majority, they too agreed that the perks offered in HOC 2021 is off to a good start, and believes that with moderate tweaking and improvement, the initiative may actually be able to help the economy.

Our take

As the old adage goes, “Fortune favors the prepared,” we firmly believe that HOC 2021’s reintroduction into the market will significantly benefit those who are looking to buy a property, provided they have done their homework and due diligence.

Presently, Malaysia has only organized HOC four times. Once in 1988 and 1999, followed by a resurgence in 2019 and now 2021. In its three previous appearances, the HOC’s sole purpose was to curb property overhang.

Today however, its main objective as a part of PENJANA is to prevent the economy from slumping further. Consequently, this has motivated the government to introduce additional perks to the initiative to encourage more property players to level the playing field.

Between MCO, the Covid-19 pandemic and everything else that has affected our country so far, HOC 2021 is still a boon for many Malaysians despite what some experts may posit. And its limited appearance is proof enough of that.

To prove our point, here’s a table summarizing the perks of HOC 2021.

Things to consider

Put simply, HOC 2021 is a good steal and we encourage interested parties to make their move soonest if they can, as the initiative won’t be around for long and there is no promising that some of the perks may return in its next iteration.

Now that we’ve gone over HOC 2021 briefly, it’s time to talk about the preparations you should make leading up to your HOC application.

Ensure your developer is registered under HOC

Although HOC 2021 is already boasting an impressive list of developer names under its belt, there are bound to be names out there that are left out. To err on the side of caution, you should check with either REHDA, 社达, or 共享 to determine if your property developer is included, which you can do so by clicking on the names itself above.

Take note of HOC’s running period

HOC 2021 is scheduled to last from 1 June 2020 – 31 Dec 2021, which means you should purchase your property during the given timeframe to qualify for HOC’s benefits. Any properties purchased prior to that will be disqualified from the process, sadly.

Furthermore, you need to ensure that any properties purchased throughout the period should also not be subjected to any government price control.

Check your DSR and Credit Scores

Self-explanatory. Banks will be looking at your scores throughout this period to determine if you are eligible for a housing loan. As such, it might be good to check with your preferred or go-to bank on your current financial standing, as that would give you an idea of how likely you are to receive any loans.

Identify the necessary documents

HOC 2021 comes with its own stringent list of conditions that individuals have to prepare before they can qualify for the program. Some of the commonly required documents will no doubt involve

身份证

Latest 3 months of payment slip

最新EPF声明

Letter of employment to name a few.

The list of document also extends to the developers, i.e. Certificate of Completion and Compliance (CCC) and a valid Developer’s License (DL). We have an article that covers HOC 2021 on an in-depth level, so feel free to head over这里 if you wish to learn more about the initiative and the procedures.

结束语

The very purpose of HOC 2021 and PENJANA is to help drive Malaysia economy forward following the brunt of MCO and the pandemic. With the property market being one of the key sources to generate revenue for the country and the public, the government will no doubt tap into it to help tide through the financial storm.

That said, they are also acutely aware of the financial hardships that many Malaysians face these days. As such the government has gone to further lengths to increase the appeal of HOC 2021, in hopes that it will make fellow homebuyers’ financial sacrifice worthwhile.

总结

HOC 2021 boasts a number of benefits that makes it an extremely good steal, thanks to the PENJANA plan. Considering the time that we live in, the benefits provided by the initiative is quite frankly godsent. If you have plans to get a home and you also happen to possess the necessary financial resources to do so, perhaps now would be the best time to make hay while the sun shines.