So you’ve received your MM2H visa, you now hold most rights that the average Malaysian is entitled to. The lengthy process is over, and now it’s time to move on to property buying. Where do you start?

Governing law for foreigners buying property

First things first, any foreigners hoping to purchase any kinds of property in Malaysia is defined as foreign interest. The definition includes:

Individuals who are not a Malaysian citizen

Individuals who are permanent residents

Foreign company or institutions

Local companies wherein 50% of the voting rights belong to a foreign party relating to point 1 – 3

As a foreigner in Malaysia, your property buying shenanigans are subjected to the following limitations as listed under the Guideline on the Acquisition of Properties.

You may not purchase any properties valued at RM1,000,000 or below

You may not purchase any low or low-medium cost houses as determined by the State Authority. This includes affordable housing schemes such asRumah Selangorku,PR1MA andRUMAWIP to name a few

Properties built onMalay Reserved Lands

Properties meant for Bumiputera folks in any property development project as designated by the State Authority.

The types of property you can purchase

While foreigners face limitations in the department of the price range, they are able to purchase all types of property so long as it keeps to the conditions above. This includes:

Landed properties

Condominiums

Apartments

Flats

Serviced apartments and SOHO intended for residential use

Residential units

Industrial property

Studio unit

Commercial property

In a nutshell, foreigners can purchase any property types on Malaysia property market. They must not violate the minimum price purchase limit set; Nor should it violate any property rules/laws catered to specific individuals or ethnicities. Yes, that includes sub-sale purchase of properties.

Time to buy a property

Foreigner or not, the process to buy a property in Malaysia largely remains the same. You will have to apply for housing loans, pay the additional costs involved and be prepared to face the possibility of having your application rejected.

The differences lie in the numbers and figures involved, with a few extra steps, usually concerning paperwork thrown into the mix.

State authority consent

The consent here refers to the state that is in charge of passing the foreigner’s rights to purchase a home. This is in accordance withNLC 1965, Section 433B which deems that prior approval must be obtained from the relevant State Authority for any acquisition of property by a non-citizen or a foreign company. Essentially, to buy a property, you must first have the state government’s approval.

To do that, you will have to obtain a set of forms from the relevant state government’s office, fill it up and pay a sum of the application fee to obtain approval. The paperwork, charges and time it takes to process your application vary between state government to state government, so there is no hard-and-fast timeline to the process.

Generally, as long as you submit the necessary documents stated in the application and pay up the fees, the approval should come along easily.

EPU approval

EPU approval only comes into the picture for two reasons.

The direct acquisition of a property is valued at RM20,000,000 and above which results in the dilution in the ownership of property held by Bumiputera interest of government agency

The indirect acquisition of a property by other Bumiputera interests through the acquisition of shares leading to a change of control of a company owned by a Bumiputera interest and/or government agency. This property represents more than 50% of its total assets and worth more than RM20,000,000.

Put simply, unless your purchased property exceeds the value of RM20,000,000 there is no need for you to obtain approval from EPU.

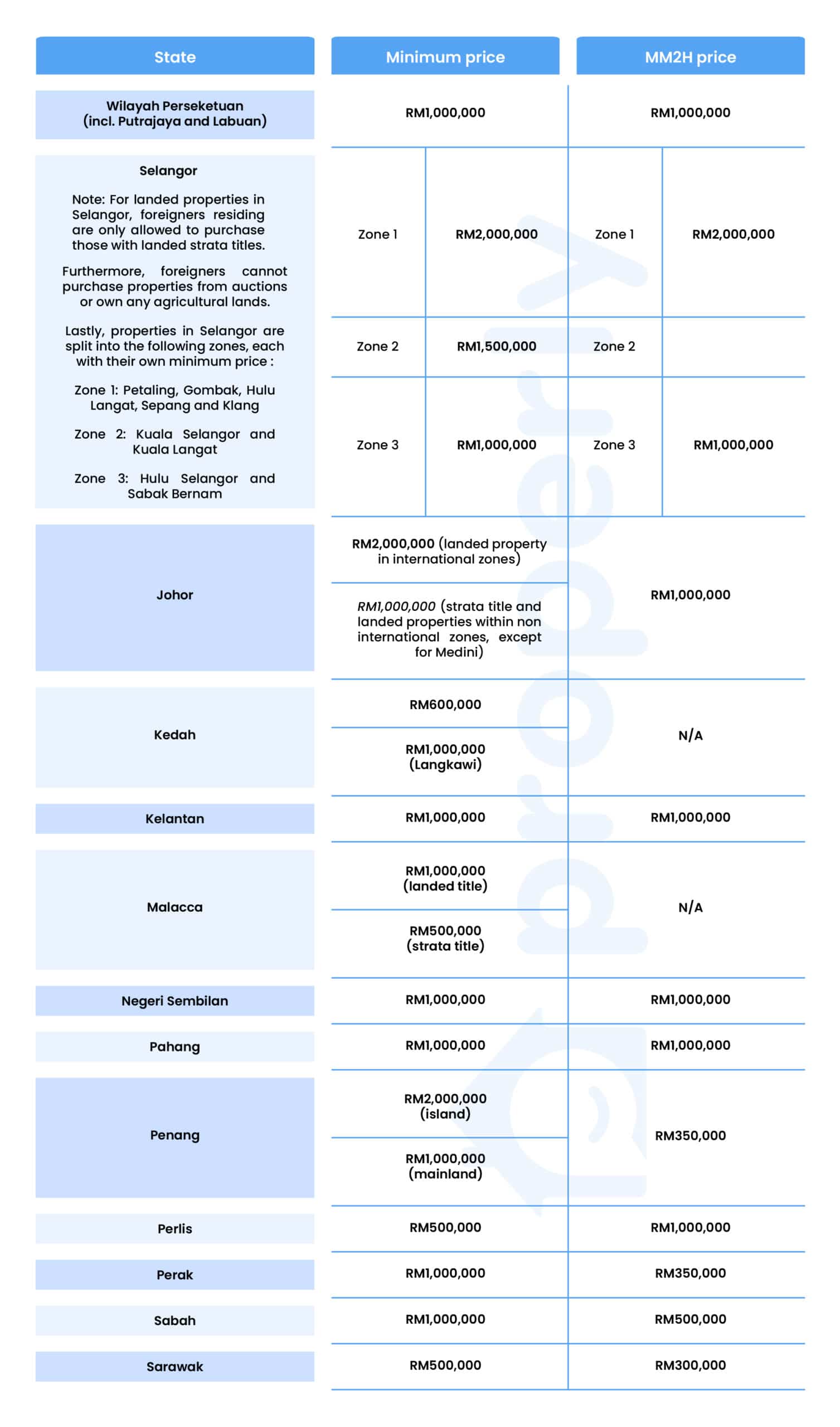

Number and figures

It should come as no surprise that foreigners are required to pay more when purchasing a home, owing to the fact that they have a minimum price limit to adhere to. This minimum price limit varies from state to state, as does the additional costs such as stamp duties and door tax & title fees.

Minimum price limit

References courtesy of LoanStreet and iProperty

Unfortunately for some states, having a MM2H visa does not grant its holders access to lower minimum prices, and in a case like Perlis, the price increases instead. That said, having a MM2H visa is a prerequisite not just for buying a property in Malaysia, but also to settle down in the country for an extended period of time. Foreigners will just have to consider the property prices and tradeoffs that may come with certain states under MM2H.

Stamp duties & legal fees

Stamp duties are taxes in the form of legal documents to officiate and formalize the transfer of an asset (property) from developer to buyer, and buyers are taxed a certain amount upon successful purchase of a property.

Stamp duties are important for two reasons – One, they are proof of home ownership for the buyer. Two, they serve as a form of legal evidence to be presented before the court if any property disputes were to arise.

The process involves the expertise of a lawyer to vet, and as such, foreigners will have to pay for legal fees too.

Stamp duty costs

There are two forms of stamp duties involved in the transaction.

Instrument of Transfer and Instrument on Loan Agreement

Sales and Purchase Agreement (SPA)

Depending on your property prices, you will be taxed according to these numbers.

wdt_ID

Property Prices

Amount Taxed

1

First RM100,000

1%

2

RM100,001 – RM500,000

2%

3

RM500,001 – RM 1,000,000

3%

4

>RM1,000,001

4%

Legal fees

Meanwhile, for legal fees, these will be the amount involved.

wdt_ID

Legal Fees

Amount Taxed

1

First RM500,000

1% (subject to a minimum fee of RM500)

2

RM501,000 – RM1,000,000

0.8%

3

RM1,000,001 – RM3,000,000

0.7%

4

RM3,000,001 – RM5,000,000

0.6%

5

RM5,000,001 – RM7,500,000

0.5%

6

>RM7,500,0001

Negotiable and subjected to a ceiling price of no more than 0.5%

Taxes and service charges are imminent in most cases. At first glance, these additional costs can put most people off. As a foreigner, they may even feel like a strange concept to you. But these are the necessary evils you will have to go through when purchasing a property in Malaysia.

Getting a home loan

The government acknowledges the higher property prices and costs that foreigners are expected to bear. In light of that, they’ve made housing loans accessible to foreigners to help ease their financial burdens too.

Margin of Finance (MoF)

Foreigners attempting to apply for a housing loan in Malaysia will find that they have a solid number of options to pick from . Generally, these loans can be applied through international banks or onshore banks unless stated otherwise. You could also check Malaysian banks that have been listed and approved by Malaysian government. Additionally, you should take note of the Margin of Finance, or MoF that is set for foreigners.

MoF refers to the amount of financial backing a foreigner is likely to receiveFtypeFF from the bank, which is where MM2H starts to shine. Under the MM2H program, most banks will offer foreigners with 80% loan, as opposed to the standard 70%. An interesting thing to note is if your spouse happens to be Malaysian, you can potentially receive a 90% loan, provided your spouse (can acts as citizen sponsor) has a part in the loan financing too.

Apart from that, holding a MM2H visa means most banks are more inclined to greenlight your loan request too, as it serves as a form of reassurance and validity for them.

Meanwhile, the terms and conditions to applying for a housing loan are as follows:

Ensure tenure is no more than 30 years

Applicant must clear off the loan by no later than 70 years of age

As far as the variety of housing loans go, you will have access to Islamic or Shariah-compliant loans too, especially for foreigners hailing from Islamic countries. If you are not a MM2H visa holder, securing a housing loan may prove to be a bit of a challenge for you, and in most cases, banks will typically recommend getting a loan from your home country to pay off your housing loans in Malaysia instead.

On a final note, housing loans for foreigners usually involve base rates, meaning you’ll be charged a price as per the central bank’s rate plus an additional percentage. If you would like to know more about base rates, we encourage you to givethis article a read.

Famous property hotspots in Klang Valley

Now that we’ve gotten the numbers out of the way, it’s time to divert our attention to locations for a bit. When it comes to buying a property in Malaysia, or at least Klang Valley, you will generally be looking at properties located within the heart of the city itself, or properties that are situated in affluent neighborhoods strategically situated right on the fringes of Kuala Lumpur.

Here are some locations you should keep your eyes peeled for a potential home.

Golden Triangle (Bukit Bintang, KLCC, Changkat)

An area that is situated right next to the Central Business District, an area where a conglomerate of large corporations is located. This place is known for its utmost centrality, with access to various large and high-end shopping malls such as Pavilion, KLCC and Fahrenheit. Even at night, the area is never short of exciting nightlife activities and fun. Foreigners who prefer an urban lifestyle will feel most at home here, with property prices boasting contemporary designs and fetching a minimal price of RM1,000,000 minimal. Perfect for individuals who enjoy the finer things in life. Here are some examples of properties that one can find in the heart of Kuala Lumpur.

Mont Kiara

A high-end area located just outside the fringes of Kuala Lumpur. Mont Kiara is known for its extremely diverse expatriate community. It is perhaps best known for its mini-Korean and Japanese community, and offers its very own unique nightlife activity within the area too. Individuals who prefer living slightly away from the hustle and bustles of the city center yet finding themselves wanting a neighborly environment will settle down just nicely in the area. A plus point of Mont Kiara is it is situated very close to an urban neighborhood in Selangor, Petaling Jaya.Property prices here begin at RM500,000 minimal, and can scale up to RM1,000,000 – RM3,000,000 on average.

Bangsar/Damansara Heights (Bukit Damansara)

A close rival of Mont Kiara. Bangsar and Damansara Heights offer its own unique nightlife to its inhabitants. High-end bars and restaurants are a common sight in the area; and the houses are nothing short of amazing. Considered one of the older locations in Kuala Lumpur, the houses in these areas boast a more traditional design. It is more well-acquainted with retirees and those who prefer a quiet suburbia lifestyle. Don’t let their quaint outlooks fool you though, particularly the landed properties, as one semi-detached can easily set you backRM2,000,000 minimal.

Bukit Tunku

Dubbed as the Beverly Hills of Kuala Lumpur. Bukit Tunku is an extremely old yet serene area that features houses the size of a mansion, with luscious forest surrounding the area. Touted as one of the up-and-coming entertainment hubs for young Malaysians, Bukit Tunku has seen a surge in attention over recent years, with some developers setting their sights on Bukit Tunku soils for a potential development project.Houses here fetch an average price of RM2,000,000 each. Much like the aforementioned areas, Bukit Tunku enables its inhabitants access to a plethora of hot spots within Klang Valley, owing to its centrality.

Honorable mentions

The list of high-end areas in Klang Valley are endless and unfortunately, it would be impossible for us to cover all of them. That said, there are many areas in Klang Valley worth looking at; here are some names to get you started.

Bandar Utama (specifically Tropicana Golf Club)

Damansara Perdana

Taman Tun Dr. Ismail

Damansara Utama

Subang Jaya

Sunway

Shah Alam

Petaling Jaya (specifically Section 16)

Barring Taman Tun Dr. Ismail, the areas listed here are trendy places in Selangor that have seen a decade-long surge in population. Although these areas are located further away from the city, they are self-sufficient areas in their own right, making them an ideal location for people to flock to and settle down.

The final hurdle

By now, we hope that you would have a modicum of understanding in purchasing a home as a foreigner in Malaysia. Once you’ve obtained state authority consent and done your homework on property buying, it’s time for you to overcome the hurdle – Putting your plans into motion and sealing the deal!

Submit aLetter of Offer stating your intent to purchase a property, and make an upfront payment, or earnest deposit (2-3%) based on property’s total price

If necessary, apply for a housing loan

Submit the relevant documents to your lawyer for processing purposes

A SPA will then be given in 14 days, followed by a 10% down payment for the home. The 2-3% previously paid will contribute to the 10% too, meaning you would have a remaining 8-7% to pay up

A final state authority consent will be needed. Foreigners are required to submit the following documents to seal the deal

One certified true copy of SPA

One certified true copy of your passport

Latestquit rent assessment receipt for property

Application form as per 433B of National Land Code

For foreign companies, one certified true copy of company constitution will be required

Proceed to paying your home loans on a monthly basis

Receive strata title from developers within 24-36 months

And there you have it, you are finally a full-fledged homeowner in Malaysia! All that’s left is to renew your MM2H visas on a 10-yearly basis, and continue paying your home loans on time.

Termination of MM2H visa

Sometimes, things happen and you may be forced to cut things short. Let’s say you’ve decided to cancel your MM2H visa before its 10-year expiry date for some unknown reason(s), and now you would like to understand what the termination process entails. That can be done too.

In this case, the termination of your visa will be conducted via two channels – Through the Malaysian Missions Abroad or at the Malaysian Immigration Department.

Malaysian Missions Abroad

Applicants must be present at theMalaysian Missions Abroad to express their intention to terminate their MM2H visa

Applicants will be asked to present the following documents

Letter of Intent for Termination of MM2H visit pass

A copy of Conditional Approval Letter

Passport with MM2H visa

A copy of termination letter supplemented by the Ministry of Tourism

Applicant must ensure MM2H visit pass is manually revoked by the Malaysian Missions Abroad

Malaysian Immigration Department

MM2H holders may request the MM2H Unit, Visa, Pass and Permit Division to terminate their MM2H visit pass in person, or email them to terminate it

Applicants will be asked to present the following documents

Letter of Intent for Director General of Immigration

A copy of Conditional Approval Letter

A copy of MM2H pass manually revoked by Malaysian Mission Abroad

A copy of termination letter supplemented by the Ministry of Tourism

But wait, what about your house in Malaysia? That’s a good question.

Selling off your property

Selling off your property as a foreigner in Malaysia is something that is relatively unheard of, given most foreigners who settle down in the country plan to do it for good. Plus, most wouldn’t dare dream of purchasing a big-ticket item, only to walk out of it in a few short years. Still… It is something that has happened before and it would be wise for us to talk about it briefly.

Selling your property is known as disposal of property, and whenever disposal of property is concerned, Real Property Gains Tax (RPGT) usually comes into the picture too.

RPGT

RPGT is applied to subsale properties, meaning properties that are sold from owner to owner, as opposed to developer to owner. RPGT is taxed whenever an owner has successfully sold off their property, and in a foreigner’s case, this is the amount taxed.

wdt_ID

Age of property

Amount taxed

3

Below 5 years

30%

4

Above 5 years

10%

Disposing of your property

Foreigners will go through the same process as per the usual Malaysian when selling off their property. The process can be broken down into these few steps:

Getting a property agent to evaluate and sell the home on your behalf

Contracting a lawyer to help with the legal procedures

Advertise your home

Provide viewings to potential buyers

Preparing a Letter of Offer

Preparing a SPA

Paying off RPGT upon a successful sale

Once all that has been concluded, all that’s left to do is to see your remaining matters before you depart from Malaysia.

Present: MM2H

We hate to be a killjoy but as of this time of writing, MM2H is currently suspended by the Ministry of Tourism and returned to the drawing board until further notice. The decision to withdraw the program was announced by the Ministry of Tourism back inAugust 2020 in light of the rising Covid-19 numbers, leading the government to bar foreigners from entering the country.

That said, the program is expected to make a comeback sometime in 2021, so stay tuned for further updates!

Summary

The MM2H program is designed to capture the attention of foreigners in hopes of enticing them to come forward and settle down in our home country, either for business or pleasure. By offering attractive benefits of residential properties such as non-taxable income and the freedom to work part time/study full time here.

Foreigners, particularly the ones relocating from developed countries, will find themselves securing an extremely good bargain from the program. For those who earn powerhouse currencies such as USD and GBP looking to get away from the hustle and bustles of their own home, buying a home in Malaysia is easily an attractive option for them. And hopefully… it will be a place where they can truly call a second home.

The information on this website is subject to change at any time without prior notice from Properly. Quantitative metrics are taken and used based on recency at the time of writing. While the Properly team takes information accuracy seriously, we are not liable for any losses due to incorrect information. The information provided is solely to inform users and is not in any way a form of offer or contract unless stated otherwise.

A high-end area located just outside the fringes of Kuala Lumpur. Mont Kiara is known for its extremely diverse expatriate community. It is perhaps best known for its mini-Korean and Japanese community, and offers its very own unique nightlife activity within the area too. Individuals who prefer living slightly away from the hustle and bustles of the city center yet finding themselves wanting a neighborly environment will settle down just nicely in the area. A plus point of Mont Kiara is it is situated very close to an urban neighborhood in Selangor, Petaling Jaya.

A high-end area located just outside the fringes of Kuala Lumpur. Mont Kiara is known for its extremely diverse expatriate community. It is perhaps best known for its mini-Korean and Japanese community, and offers its very own unique nightlife activity within the area too. Individuals who prefer living slightly away from the hustle and bustles of the city center yet finding themselves wanting a neighborly environment will settle down just nicely in the area. A plus point of Mont Kiara is it is situated very close to an urban neighborhood in Selangor, Petaling Jaya.