You’ve most likely heard about B40, M40, and T20 in the news many times recently, especially when it comes to receiving financial assistance amid the Covid-19 pandemic, but what do they actually mean, and where do you stand? This is an important terms that all Malaysians should know about.

What are B40, M40, and T20?

Basically, these refer to income groups in Malaysia, where Malaysia’s population is classified into three different groups based on their household income – B40 represents the bottom 40% of income earners, M40 represents the middle 40%, and T20 represents the top 20%.

In other words, these income classifications split earners into different classes such as poor, lower-middle-class, middle class, upper-middle-class, and wealthy to help the government determine how to allocate social aid programs and formulate national economic plans.

Is the bar for each group’s income level fixed?

It is important to keep in mind that these income group definitions are not fixed. The values may increase or decrease year-to-year, depending on the country’s economic growth.

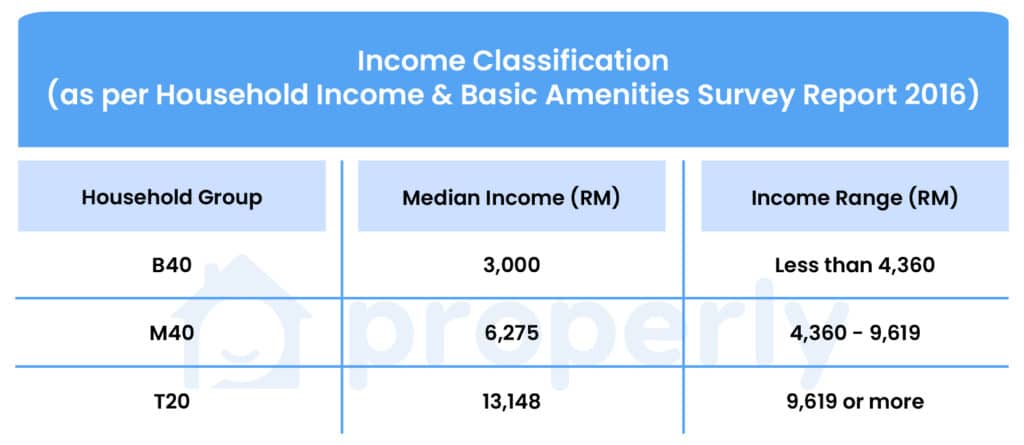

Previously, based on the Department of Statistics Malaysia’s (DOSM) Household Income & Basic Amenities Survey Report 2016, the median household income for each of the B40, M40, and T20 groups are pinned at RM3,000, RM6,275, and RM13,148 respectively.

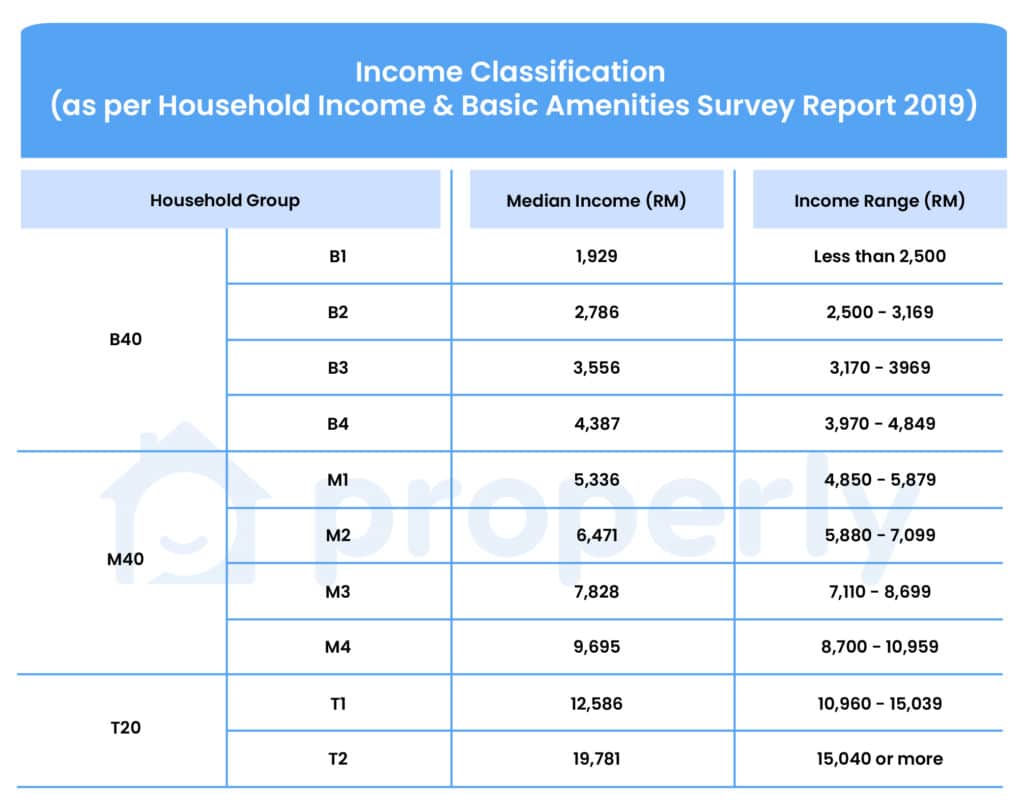

In 2019, the survey report by DOSM shows that the median income for each of the B40, M40, and T20 groups has shifted higher as compared to the 2016 figures, amounting to RM3,166, RM7,093, and RM15,021 respectively. These figures show that household incomes are growing over the years without taking into account the general economy, with the T20 tier seeing the largest increase in their incomes.

Besides, the B40, M40, and T20 income groups are further classified into a total of 10 sub-categories based on the latest 2019 Household Income Survey by DOSM, such as B1, B2, B3, B4, and so on – as compared to the 2016 report without the sub-categories. These figures are revised to be more impactful and precise in reflecting the escalating cost of living, living wages, inflation, and household size amongst other factors.

Check out the table below for a clearer picture of the income threshold and median incomes of the new classifications:

Based on the report – to know which income group your household belongs to – the income threshold for Malaysia’s B40 group of about 2.91 million households was RM 4,849 – which means households with earnings below RM4,850 per month in 2019 were considered B40.

The M40 group comprising another 2.91 million households are those that earn between RM4,850 to RM10,959 per month, while the remaining 1.46 million households earning more than RM10,960 per month are considered in the T20 tier.

National income distributions

Interestingly enough, T20 possesses 46.8% of the national income share (higher than 2016’s ratio of 46.2%), M40 has 37.2% of the national income share (lower than 2016’s ratio of 37.4%), while the B40 gets 16.0% of the national income share (lower than 2016’s ratio of 16.4%). This highlights the worsening income inequality in Malaysia with the top 20% of income earners generating almost half of the total household income in Malaysia.

Income inequality

Based on the Khazanah Research Institute’s (KRI) State Of Households 2018 report, the country’s household income has steadily increased since 1970, while the Gini coefficient – which measures income inequality – fell from 0.513 to 0.399. Simply put, a lower Gini coefficient value means the income inequality is lower.

This means that in the past few decades, household income has risen, and income inequality has declined. However, the Gini coefficient value increased to 0.407 in 2019, compared to 0.399 in 2016. This shows that income growth has become less inclusive as income inequality has widened in recent years.

The State Of Households 2018 by KRI also revealed a steady increase in the income gaps between the T20, M40, and B40 groups since 1970. The estimated real mean household income differences between T20 and M40, M40 and B40, and T20 and B40 increased to RM9,000, RM4,000, and RM13,000 respectively in 2016, as compared to the figures in 2000 at RM6,000, RM2,000, and RM8,000 respectively. This highlights that the absolute earnings gap between the Top 20% income earners and other groups nearly doubled in the two decades up to 2016.

Hence, despite the declining Gini coefficient for income distribution over the years, the general perception of the rich is getting richer, while the poor are getting poorer, becomes more visible. Indeed, the rising cost of living and low wages have put financial pressure not only on the B40s but also the M40 group – which are deemed “too rich” to receive government subsidies but “too poor” to enjoy a comfortable life in the face of the higher cost of living in urban areas.

One of the main concerns among the young M40 groups is that they can no longer afford to buy a middle-class home as they do not even earn enough in the first place. This is unlike the situation for the T20 households, which have disposable income for investment and wealth creation.

How much did Malaysian households spend?

The State of Households 2018 report by Khazanah Research Institute (KRI) revealed that lower-income households (households earning below RM2,000) spent 94.8% of their income on household expenditure with a big chunk on food and non-alcoholic beverages as a result of the need to purchase raw materials for home consumption.

However, the higher-income households (households earning above RM15,000) only spent 45% of their income on household expenses, including shifting to more aspirational lifestyle purchases such as after-school private tutoring for their children and overseas holidays.

Meanwhile, the middle-class (households earning below RM5,000) spent 67% of their income mainly on consumption items and everyday essentials, whilst facing a spectrum of trade-offs in food consumption despite spending more money on it given the rapid food-price inflation.

This highlights households earning below RM2,000 are potentially very vulnerable to any economic shocks as they will not have enough savings for emergencies. Besides, more Malaysians, including the M40 group, may find themselves among the poor in reality amid the Covid-19 pandemic, despite being considered the country’s middle-class from the official M40 classification.

This is why the government’s economic stimulus incentives have always focused on improving the B40 and M40 groups’ purchasing power to boost domestic spending, which includes making homeownership more accessible too.

Below is a list of some affordable housing schemes in Malaysia, especially for first-time buyers:

Residensi Wilayah (RUMAWIP)

Residensi Wilayah, formerly known as RUMAWIP, is an affordable housing program by the government (Kementerian Wilayah Persekutuan) to help lower and middle-income groups across the Federal Territories of Kuala Lumpur, Putrajaya, and Labuan to own their first property.

Scheme details:

Low-price houses sold at RM63,000 per unit in Kuala Lumpur and Putrajaya, while they sold at RM52,000 in Labuan.

Maximum cost of RM300,000 per property.

Units have a built-up size of no less than 650 sf.

10-years moratorium imposed where the purchased house cannot be transferred or sold to a new owner without the government’s permission, unless to the closest family members or heirs like spouses or children only.

10% deposit requirement of the total unit price upon successfully obtaining a Residensi Wilayah unit.

Owners can rent out their properties to a third party but on a certain term.

Eligibility criteria:

Applicants must be Malaysian citizens of at least 21 years old.

Priorities are granted for those who were born, work, or live in any Federal Territories upon application.

Priorities are given to those who do not own any property in the Federal Territories area.

Gross income for individual applicants must not exceed RM10,000 per month; while married couples must have a total income of no more than RM15,000 per month.

The Perumahan Penjawat Awam Malaysia (PPAM) scheme, also known as the Malaysia Civil Servants Housing Programme, was designed to help government civil servants, particularly low, middle-income civil employees, to afford their own homes in major urban areas.

Scheme details:

Attractive units ranging from RM90,000 to RM300,000, with a variety of unit types including landed and high-rise.

The owner must not rent out his or her home after acquiring a unit.

No resale for the first ten years, except to the next of kin or with the government’s permission to do so.

2% deposit required upon signing the Sales and Purchase Agreement (SPA).

A unit sold to the buyer cannot be changed once the offer is confirmed.

Once an offer is made, buyers will have up to two months to secure their financing.

Eligibility criteria:

Applicants must be Malaysian citizens and reside in Malaysia.

Must be a civil employee who works in Federal Government, State Government, State Authorities, Local Authorities, Federal Statutory Bodies, and State Statutory Bodies.

Have a monthly income below RM10,000.

Priorities are given to first-time buyers.

Only one successful project per household.

Pensionable and contracted civil servants are also eligible to apply.

The My First Home Scheme is an initiative that was first announced by the government in the 2011 Budget to assist first-time homebuyers who earn below RM5,000 per month individually, or below RM10,000 a month as a household, to purchase their first home.

Scheme details:

Maximum property value of RM500,000

Up to 110% financing

5-years moratorium period

Owners are required to reside in the property

Instalments payable via monthly salary deductions or standing orders

Maximum loan term not exceeding 35 years, subject to applicant’s age not exceeding 70 years at the end of the term.

Eligibility criteria:

Applicants must be Malaysian citizens

Must be a first-time buyer

Available for salaried worker or self-employed individuals

Single or joint applicants allowed (joint applicants must be immediate family members)

No record of impaired financing, such as failure to repay loans, within the past 12 months

PR1MA (Perumahan Rakyat 1Malaysia/1Malaysia Housing Programme)

PR1MA housing program was established by the government to help middle-income households looking to buy a home in key urban centres in Malaysia. The properties are offered via an open ballot, registering for PR1MA housing is absolutely free!

Scheme details:

Property prices between RM100,000 to RM400,000.

Properties are available in various locations and states across Malaysia.

A 5-year moratorium is imposed on the property, during which it cannot be sold or transferred without approval from PR1MA.

The property must be owner-occupied without subletting.

Eligibility criteria:

Open to all Malaysian citizens, single or married.

Applicants must be aged 21 and above at the time of application.

Individual or combined (husband and wife) monthly household income between RM2,500 and RM15,000.

Does not own more than one property, between them and their spouse.

Rent-to-own (RTO) schemes are an alternative to traditional home loans. This model requires one to rent a residential unit, which differs from 12 months to 5 years, with an option to buy the property in the future at an agreed locked-in price or walk away without any obligation.

One of the main attractions of RTO is that no down payment is required. In other words, RTO can be thought of as a trial period for a buyer to experience living in the property he or she desires without forking out a hefty 10% down payment and additional transactional fees upfront.

A buyer will only need to prepare a security deposit of three months’ rent, and part of the monthly rent they pay will be credited to the property’s future purchase in the form of savings accrued to settle the down payment if a buyer decides to buy. They can be attractive to buyers, especially those who are still building their credit scores and expect to be in a stronger financial position within a few years.

Check out some of the better-known RTO schemes available in Malaysia:

Maybank HouzKEY

Photo: Maybank2u

HouzKEY is a homeownership financing solution introduced by Maybank to assist young couples and adults looking to own their first home but lack sufficient funds for a down payment. Maybank’s HouzKEY home loan is designed to assist homebuyers in their home financing with great flexibility and cash flow efficiency.

Scheme details:

Up to 100% financing including incidental costs such as legal fees and stamp duty among others.

0% down payment and no payment during construction.

The buyer only pays a three-month security deposit to secure a property.

A locked-in property price and lowest monthly payment.

Eligible for new launches, under construction, or completed properties located across Selangor, Kuala Lumpur, Johor, and Penang.

Eligibility criteria:

Applicants must be Malaysian citizens.

Applicants must be between 18-70 years old at the time of application.

No more than one home financing at the time of application.

The applicant may include up to three guarantors to improve the application success rate.

The PR1MA RTO housing scheme was tabled during the Budget 2021 in November 2020 to cater specifically to first-time homebuyers. It is expected to be launched in June 2021 and the scheme will be effective until 2022.

According to the Housing and Local Government Housing Minister (KPKT) Minister, Datuk Zuraida Kamaruddin, the ministry is in the midst of discussions on the housing scheme mechanism to be adopted with banking institutions.

Once the scheme is finalised, homebuyers can expect to apply from a list of 5,000 PR1MA homes nationwide.

The Rent-to-own scheme (2STAY), led by Lembaga Perumahan dan Hartanah Selangor (LPHS), is aimed to assist the lower-income bracket segment (B40), especially those facing difficulty in obtaining bank loans to own their dream homes at less than RM200,000.

Scheme details:

A minimum rental duration of 2 to 5 years.

A 30% return of the total rental is paid and used as a deposit if the tenant can buy the property within the stipulated 5 years.

The average rental rate begins from RM600 to RM750 per month.

Eligibility criteria:

Open to Malaysian citizens only, including spouses;

Applicants must be aged 18 and above, with family/commitments;

Monthly family income level must not exceed RM5,000 a month for Type A or low-cost housing; or RM15,000 a month for Type B, C, and D properties, including affordable and low-cost housing (priorities given to those with family income below RM10,000/ month).

Applicants and their spouses must live and work in Selangor.

Applicants must not own any property in Selangor.

If applicants do own a property, it must be located more than 50 kilometers away from the applied location and within a 25km radius of their workplace.

Applicants must be registered voters in the state of Selangor.

As with most home ownership schemes, there is no one-size-fits-all. Homebuyers will need to identify their current needs and decide what is best for their pocket. For B40s, look at the bright side! The housing initiatives above are mainly aimed to help the B40 group secure their own home, some are even suitable for those M40 households fringing near the B40 threshold.

Are you ready for your homeownership journey? Find the perfect dream home and make it a reality with Properly! Submit your home requirements today and have a chat with us if you need any industry advice.

The information on this website is subject to change at any time without prior notice from Properly. Quantitative metrics are taken and used based on recency at the time of writing. While the Properly team takes information accuracy seriously, we are not liable for any losses due to incorrect information. The information provided is solely to inform users and is not in any way a form of offer or contract unless stated otherwise.