Buying a home is more than just an affair of knocking on a developer or property agent’s door and unloading your years of hard-earned money to afford one. Even if you could do that, the banks would be on your tail, in fact the government might start questioning if you’ve been declaring your taxes consistently.

Just like any other services or goods with high value out there, there are often additional costs associated with their purchase. Think getting hospitalized for example. There are a ton of costs involved apart from treatment and consultation. As a patient warded in the hospital, you are expected to pay for the hospitalization costs, equipment fees, perhaps your hospital gown and maybe even your meals assuming they aren’t included within the package.

Thus, the same analogy applies to buying a home. When you’ve decided to buy your virgin abode, you are not only expected to pay for the house but you will also be requested to cover these additional costs, known as instruments too:

Stamp duty,

Loan agreement,

Sale and Purchase Agreement (SPA),

Legal Fees,

Commission for property agent (if applicable).

Oftentimes, the sight of these additional costs can diminish our excitement. Why? Because it’s additional money spent.

In fact, you might even get upset knowing most of the additional costs revolve around a set of instruments or legal documents, in layman terms. Why on earth do you have to pay so much for a piece of paper? It all seems rather superfluous, and it hardly feels like they contribute to the actual process of home buying. But please don’t go saying that to your legal-practising friends. They will be sure to give you an earful.

In truth, these instruments play two important roles, they are:

A form of government revenue,

A form of admissible evidence to protect homebuyers from any form of exploitation in the event things hit the fan.

Still think legal documents are “superfluous”? These papers are one of the few things that stand between you and a potential house loss if things go south. Without these documents backing you up, the law will never be able to defend you. Think insurance, but for homes and in a legal sense. This brings us to our topic of the day – HOC 2021.

The Malaysian government understands forking out more money for legal documents can be a heartbreaking affair, and that is why they’ve come up with HOC 2021 to help spare you the pain. Before we go on, we have to say that anything legal related to homebuying falls under a broader spectrum.

We will be talking about stamp duties today, given its close relation to HOC 2021. Let’s begin.

Home Ownership Campaign (HOC) 2021

In order to realize what HOC 2021 and stamp duty are, one must first understand the origins of HOC.

HOC, otherwise known as Home Ownership Campaign, is an incentive started by the Malaysian government in 2019 to help curb the issue of property overhang and increase ownership of homes amongst Malaysians. The inception of the incentive program came to life when the government realized there was a surge in demand for homeownership, though the demands predominantly came from those who lacked the financial capability to afford one. In a nutshell, the government is attempting to help struggling Malaysian make their home-owning dreams come true, and that’s great because it shows they are listening.

It also helps address the issue of property overhang, which is a massively detrimental issue to the country if left unaddressed long-term. Property overhang refers to completed residential units that have been accredited with Certificate of Completion and Compliance (CCC) that remain unsold for nine months or more. In case you’re curious about the residential units inferred here, it’s the following:

Houses,

Condominium units,

Apartments,

Flats,

Serviced Apartments and SOHOs used as homes.

Why property overhang?

Property overhang is a classic case of oversupply and under-demand, meaning housing developers are raising residential units at a rate quicker than the consumers can afford to spend. This happens for a few reasons:

Poor planning by developers,

A lack of studies/Studies not accurately reflecting the property market and Malaysians’ buying power,

Poor coordination among local authorities during the building process,

A delay in local plans, which results in further development,

Artificial demands,

Higher cost.

At the risk of sounding as if we’re picking sides, the issue of property overhang is perfectly understandable, seeing as developers are merely trying to make a living. The jarring problem here is that past studies have inaccurately reported on the situation, which results in unsold properties piling up over time. Property overhang is fundamentally serious for one simple reason – It incurs massive financial losses.

In Q2 2019 alone, astatistics study carried out by Nawawi Tie Leung Property Consultants Sdn Bhd estimated that 52,666 residential units in the country were unsold.

Attempting to curb property overhang

To tackle the issue of property overhang, the government teamed up with Real Estate and Housing Developers Association Malaysia (REHDA) to launch HOC 2019 to boost property sales.

Initially meant to run from 1 Jan 2019 – 30 Jun 2019 only, the effort netted the governmentRM14.65 billion worth of sales, with 19,784 units reportedly sold as of September 13, 2019. This spurred Minister of Housing and Local Government, Zuraida Kamaruddin, to extend the promotional period to 31 December 2019, resulting in further sales and further curbing of property overhang.

HOC 2019 & HOC 2021 Perks

Speaking of HOC 2019, the program offered the following benefits:

10% discount offered by developers for properties priced between RM300,001 – RM2,500,000,

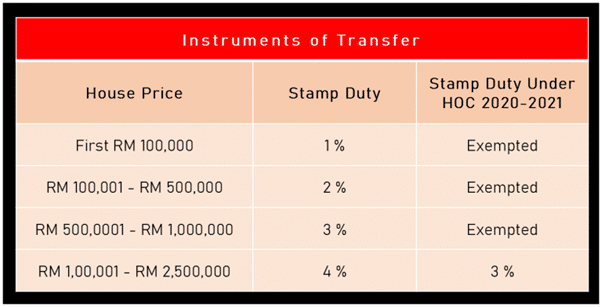

Stamp duty exemptions on Instrument on Transfer with the following conditions:

wdt_ID

Property Price

Stamp Duty

1

First RM100,000

Exempted

2

RM 100,001 – RM 500,000

Exempted

3

RM 500,001 – RM 1,000,000

Exempted

4

RM 1,000,001 – RM 2,500,000

3%

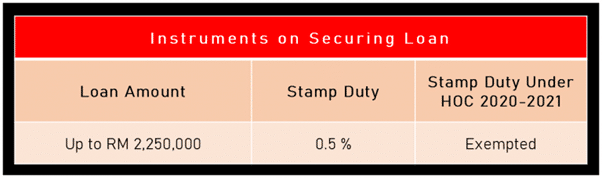

Stamp duty exemptions on Instrument on Loan Agreement/Securing a Loan

wdt_ID

Price

Stamp Duty

1

Up to RM2,500,000

Exempted

All this might sound rather theoretical and difficult to grasp, so we’ve gone ahead and provided you with a hypothetical math example.

Let’s assume that you’re purchasing a house with the following conditions:

Your house is priced at RM500,000,

You’re required to make a 10% down payment,

wdt_ID

Description

Without HOC

With HOC

1

Down Payment

[RM500,000 x 10%]

~([RM500,000 x 90%] x 10%)

2

Stamp Duty Exemption on Instrument of Transfer

1% for the first RM100,000

2% for the next RM100,001 – RM 500,000"

RM100,000 x 1%

RM400,000 x 2%

Exempted

Exempted

3

Stamp Duty Exemption on Loan Agreement/Securing a Loan

*RM450,000 x 0.5%

Exempted

4

Monthly Housing Loan (Let’s assume you pay 4% Housing Loan monthly over the span of 35 years @90% purchase price)

~10% discount offered by developers is based on the down payment price * Loan Agreement is set at a fixed 0.5% rate + down payment **Cost not inclusive of legal fees and real estate agent’s commission

To sum up the table above, an individual who registers under HOC saves a whopping RM14,198.25 if their property is priced at RM500,000, enough to guarantee them a year’s worth of rental assuming they lived in a condo in an upscale area like Mont Kiara.

If the table above is still too confusing for you, here’s an infographic to help you understand the perks better.

HOC 2019 & 2021 Perks on Instruments of Transfer. Picture courtesy of REHDA.

HOC 2019 & 2021 Perks on Loan Agreement/Securing Loan. Picture courtesy of REHDA.

In essence, HOC provides buyers exemption to stamp duty, loans and a 10% discount on top of that. Incentivizing at its best.

On a last note, if you’re looking to gauge your monthly housing loan, you can always refer to a home loan calculator designed specifically for Malaysian online. In fact, here’s one for you!

The return of HOC 2021

The onset of MCO 2020 left 729,000 Malaysians jobless and more than half of the nation struggling financially. In fact, with Covid-19 affecting Malaysia’s economy last year, the issue of property overhang became an even more predominant issue within the property market.

During the first half of 2020, report courtesy of Property Market Report H1 2020,NST reported that 32,000 units were unsold, while their value dropped from RM68.53 billion to RM47 billion. If all this is too difficult for you to understand, just know that the country suffered a loss of RM21.53 billion during the first half of 2020 from property overhang alone.

With the country’s economy heavily affected, Prime Minister Muhyiddin Yassin announced the country’s Short-Term Economic Recovery Plan (PENJANA) to help revitalize the economy. Ultimately, the plan to stimulate businesses, which would then increase buying powers and create demands among Malaysians. This is desirable because it creates a healthy economy cycle for the country. In turn, this would also lead tothe return of HOC 2020-2021.

Originally scheduled to run from June 2020 to May 2021, the government recently announced its extension toDec 2021 instead, upon realizing that the promotional period was too short a timeframe for Malaysians to recover and make any possible plans to purchase property.

There isn’t much to say about HOC 2021. Virtually all benefits and perks offered in HOC 2019 have also made its return to HOC 2021, which means those applying for HOC 2021 will enjoy the same benefits as the ones in 2019.

Also, before we forget, here’s what stamp duty for property looks like.

Let’s talk about eligibility. Despite its rather straightforward information, one has to meet a moderate list of criteria/conditions in order to qualify for HOC 2021. So it’s imperative that we talk about it.

For starters, individuals signing up for HOC 2021 will have to take note of the following criteria:

The exemption period only takes place between June 2020 – Dec 2021,

Only residential units (refer to HOC 2021 for definition) accredited withDeveloper’s License & Advertisement and Sale Permit (APDL), or CCC qualify for the exemption,

Property prices must fall within the ranges of RM300,001 – RM2,500,000,

Property purchased must occur in a developer à buyer fashion, meaning buying from secondary market or friend –> friend fashion does not apply,

The stamp duty exemption only applies to properties purchased between June 2020 – Dec 2021,

The 10% discount from developers applies to all unit not subjected to government price control,

Properties in Peninsular Malaysia eligible for HOC 2021 must be registered underREHDA,

Properties located in Sarawak must be registered underSHEDA instead,

Ditto for properties in Sabah, SHAREDA.

On a final note, homebuyers wishing to ascertain if their home developers are registered under HOC may do so here for REHDA, SHEDA, and SHAREDA respectively.

HOC 2021 – The miscellaneous

As mentioned at the start of the article, numerous additional costs have to be taken into consideration before one settles on purchasing a property. Apart from the stamp duties covered within HOC, the miscellaneous here refers to additional factors such as legal consultation fees, Sales and Purchase (SPA) Agreement and real estate agent’s commission to name a few. While we won’t be talking about these on an in-depth level in the article, we do feel the need to caution readers about them.

Sadly, most miscellaneous costs aren’t covered under HOC 2021 and homebuyers will have to clarify these additional factors with the developer or their lawyer just to be sure that everything has been taken care of. Depending on the channels in which you purchase your home, i.e.: through a property agent or directly from the developers, factors such as the real estate agent’s commission may or may not come into play.

Legal fees come into the picture when one drafts the help of a lawyer to help with stamp duties or any form of agreement, at which point you may or may not expect yourself to fork out additional fees for legal advisory services. Some lawyers are kind enough to bundle everything together, and others not so. At the end of the day, it all falls onto homebuyers to clarify these issues on the spot to ensure that they’re well in the know before committing themselves to a lifelong worth of home loans.

Other informed Malaysians, however, may choose to take matters into their hands and sort out stamp duty themselves viaSTAMPS, an online portal by LHDN which allows users to apply for a stamp. This saves time and is extremely cost-effective, though users may have to spend a considerable amount of time doing their homework before doing it themselves, lest there may be many errors that ruin the entire effort of stamp duty.

Summary

Forking out additional costs can always be a stressful affair for first-time homebuyers. After all, buying a home alone can fetch a whopping price. Thankfully, the introduction of HOC 2021 helps to do away with some of the stress, leaving first-time homebuyers with some breathing room.

FAQs

What is HOC 2021?

HOC 2021, or Home Ownership 2021 is an incentive program designed to encourage Malaysians to purchase their very own property by offering stamp duty exemptions on Instrument of Transfer and Instrument on Loan Agreement/Securing A Loan.

How long is the duration of HOC 2021?

HOC 2021 will run from June 2020 – Dec 2021.

How can my property qualify for HOC 2021?

Individuals wishing to apply for HOC 2021 will have to meet the following criteria:

Properties purchased must fall within the June 2020 ~ Dec 2021 timeframe.

Only property units accredited with APDL or CCC are eligible for the exemption,

Property prices must fall within the ranges of RM300,001 ~ RM2,500,000,

Property purchased must occur in a developer à buyer fashion, any property purchased from the secondary market will not be taken into consideration,

Properties must be registered under the following bodies:

Peninsular Malaysia → REHDA,

Sarawak → SHEDA,

Sabah → SHAREDA.

Am I only restricted to one property for HOC 2021?

There is no property cap for HOC 2021. In other words, you can apply HOC 2021 for all of your bought properties, so long as they meet the criteria above.

I’m worried my property doesn’t fall under the 10% discount promo, how can I tell if my property is included within the list?

REHDA will publish a long list of developers registered under its HOC 2021 incentive program, this means you can simply refer to the list to find out if your developer is included.

What is the exemption rate for Instrument on Loan Agreement/Securing A Loan?

Unlike Instrument of Transfer, the Instrument on Loan Agreement/Securing A Loan is subjected to a flat 0.5% * down payment rate.

The information on this website is subject to change at any time without prior notice from Properly. Quantitative metrics are taken and used based on recency at the time of writing. While the Properly team takes information accuracy seriously, we are not liable for any losses due to incorrect information. The information provided is solely to inform users and is not in any way a form of offer or contract unless stated otherwise.