Buying Auctioned Properties in Malaysia: Introduction

Buying a property, whether it is for investment or occupying, is without a doubt a huge and exciting process. One can opt to buy a new property from a developer or purchase a sub-sale property. Apart from these two traditional routes, there is another option for potential homebuyers to consider, which is to purchase an auctioned property.

On Aug 1, 2020, The Star, a Malaysian newspaper reported that 1,764 more properties were auctioned in 2019 via Lelongtips.com (a property and auto auction portal in Malaysia) compared to 2018. The same article also included a comment by CGS-CIMB Securities forecasting that the auctioned property market is likely to gain traction in the future due to factors among which are financial institutions intensifying their recovery efforts.

A property is usually put up for auction when the homeowner defaults on the mortgage payments which then leads to the foreclosure of the property by the bank. An auction is conducted by a licensed auctioneer that is appointed by the bank, or authorities such as the High Court or Land Office. During an auction, interested parties from the public can place bids on the property and the highest bidder wins.

Types of Property Auctions in Malaysia

There are two types of property auctions in Malaysia for foreclosed properties, which are:

Judicial Auctions: Also known as Non-Loan Agreement Cum Assignment (non-LACA) auctions, in these cases, the title is under the name of the borrower. The bank then applies to the high court (land registry title) or the land administrator (land office title) for an order to sell the property. The auctions will be carried out by the land court or the land administration and are regulated by the National Land Code.

Non-Judicial Auctions: These are for properties that are under a master title and the individual or strata title has not been issued. In these cases, the auction will be carried out by the bank through a private auctioneer. This is also known as Loan Agreement Cum Assignment (LACA) auctions.

wdt_ID

Criteria

Judicial Auctions (Non- LACA)

Non- Judicial Auctions (LASA)

1

Auctioneer Deposit

10%

5%

2

Period to settle the balance of purchase price

120 Days

90 days

3

Next Bidding (In the event that there is no successful bidders)

6 months

1 month

In both cases, there will be a 10% reduction in the reserve price for the second auction. The reserve price is the minimum price that the seller would be willing to accept from the buyer.

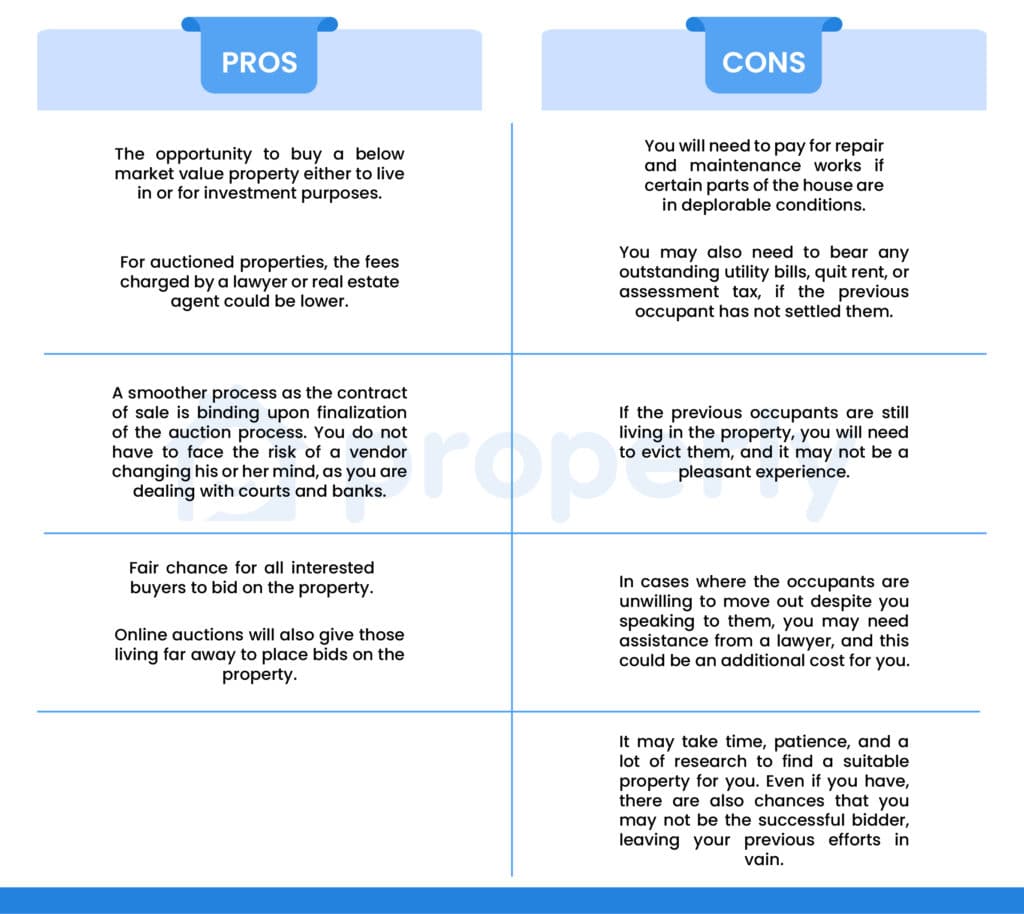

The Pros and Cons of Auctioned Properties

At this juncture, are you wondering if buying an auctioned property is a suitable option for you? Here is a simple table with the pros and cons to help you decide:

Five-Step Checklist to Help You Prepare for An Auction

If you have weighed the pros and cons and decided to purchase an auctioned property, here is a simple five-step checklist to assist you with your preparation for an auction:

1.Identification of the property

To begin, you must first identify a property that you can place your bids on and one that suits your liking. The list of auctioned properties can be obtained from newspapers or via auction platforms.

2.Investigation about the property

Once you have identified the property, it is time to do a title search of the property. Among the information you can get from doing the title search are such as particulars of the title such as the area, dimensions, and boundaries of the property, status of the title (freehold or leasehold, and remaining tenure of lease if it is a leasehold property), and if there are any charges or caveats.

Additionally, you should also obtain the Proclamation of Sale (POS) or Conditions of Sale (COS) from the auctioneer or solicitor acting on behalf of the auctioning bank to gain more information on the property. Through the POS, you will be able to know the reserve price of the property and the amount of deposit you will need to prepare.

It is also prudent to take note of the remaining years on a lease if the property has a leasehold tenure. This is because some banks might not grant you a loan for properties that have lesser years remaining on their lease, or even reduce the loan tenure. You will also need to check if the property title has been issued.

If it hasn’t, it is best to confirm if the developer has been wound up to avoid any complications in transferring the title to you. If you are not a Bumiputera, you should also confirm if the property is allocated as a Bumiputera lot.

Do also pay attention if there are any existing restrictions or caveats on the property. A caveat is a type of statutory injunction to stop the registration of particular dealings of a property. If you purchase a property that has a caveat, you must go through the process to challenge the party who submitted the caveat of the property. Until the caveat is removed, you may find it a challenge to obtain a loan from the bank.

Therefore, you will then need to ensure you have sufficient cash in hand to pay the balance if you are unsuccessful in obtaining a loan. However, even then, you must factor in the extra legal cost you will have to bear in the process of challenging the party who submitted the caveat.

By gaining sufficient information on these areas, you will have a better idea if the property will be worth your money and time.

3.Inspection of the property

It is also always prudent for you to personally inspect the property to determine the condition of the property, as well as the surrounding properties. You can also speak to the neighbours to understand the area from a first-person perspective. However, if you are unable to visit the property, you can get in touch with the sales agent or auctioneer to obtain additional information you need on the property.

For cases where you are unable to inspect the property, it would be prudent to allocate a certain amount towards the repair cost of the property, bearing in mind that most houses end up in foreclosure because the owner could not pay the monthly instalments and would have even less to repair the house. Additionally, it is also good to compare the reserve price against the other properties in the area to ascertain if the property is a good buy for you.

4.Checking on any outstanding bills

It is also prudent to check with utility companies, management offices, or relevant authorities if there are any outstanding bills on the property such as utility bills, quit rent, or assessment tax. You may need to present a copy of the Proclamation of Sales (POS) to obtain this information.

5.Preparation of bank draft

Prior to the action, you will need to prepare a bank draft amounting to 5% or 10% of the reserve price, depending on if it is a LACA or non-LACA auction. However, you must ensure that you have the remaining balance ready as your deposit can be forfeited if you do not settle the outstanding balance within the stipulated timeline. Do take note that you are not eligible to participate in an auction if you are below 18 years old or have been declared bankrupt.

On the Auction Day

With the advancements in technology, auctions are now conducted online, apart from a physical venue.

Physical Auction

If you are attending an auction at a physical venue, it is advisable to arrive at a venue earlier, especially if you are auctioning for the first time. You may also appoint your real estate agent to attend on your behalf. Register at the auctioneer’s counter and proceed to make payment for the auctioneer’s deposit, which amounts to 5% for LACA properties and 10% for non-LACA properties. Some auctioneers require that the registration and deposit be made before the auction day, so it is best to confirm with the auctioneer about this requirement.

You will then be issued a bidder’s card with a number. The auction process will start with the auctioneer briefing about the auction process and highlight key clauses in the POS. During the bidding, raise your bidding card as an indication of your bidding price. If there are no other bids after the highest price is called out three times by the auctioneer, the bidding process will stop. Upon the fall of the hammer by the auctioneer, the property is considered officially sold.

If you placed the winning bid, you would need to sign the Contract of Sale. The stamped Contract of Sale can be collected at a later date. If there is a difference in the deposit sum between the reserve price and the successful bidding price, it must be paid after the auction. Therefore, it is best to come prepared with an additional amount of cash. The balance of the purchase price will need to be settled within 90 days (LACA) and 120 days (non-LACA).

However, if you are not successful in your bidding, you can collect your deposit after the auction.

Online Auction

You will first need to create an account with the auction portal. After your account is successfully opened, you can easily browse through and select a suitable property. Then, you can register for the auction and pay the deposit required.

Before the auction day, it is best to ensure that you have a strong and stable internet connection, as well as a quiet venue so that you will not be distracted during the auction. On the auction day, do ensure that you log in earlier so that you are calm, collected, and have enough time to read the terms and conditions.

When the auction begins, both the reserve price and amount of each bid will be displayed. If you have placed a bid and someone else has placed a higher bid, the system will notify you. If you are the successful bidder, you will receive a memorandum of sale. You will then need to sign the contract of sale and if there is a difference in your deposit amount between the reserve price and the successful bidding price, you will need to top up the difference.

This can be done personally, via online bank transfers, or bank drafts delivered by Pos Laju. Similar to the physical auction, you will then need to settle the balance of the purchase price within 90 or 120 days (non-LACA), depending on if it is a LACA or non-LACA auction.

Unsuccessful bidders will receive a refund of their deposits via online bank transfer or bank drafts delivered by Pos Laju.

Conclusion

Spending time to do some research before buying an auctioned property is an investment that will pay off for you. Instead of rushing into a purchase, get familiarised with the process by attending a few auctions beforehand. If you know of others who have bought an auctioned property, take time to speak to them and gain their advice on the dos and don’ts.

Whether it is a physical or online auction, it is advisable that you set a limit to your bidding before the auction, so that you do not get caught up in the excitement of the bidding process and exceed your budget.

Doing these simple things can help you make the most of this opportunity and thoroughly enjoy the process of buying an auctioned property.

The information on this website is subject to change at any time without prior notice from Properly. Quantitative metrics are taken and used based on recency at the time of writing. While the Properly team takes information accuracy seriously, we are not liable for any losses due to incorrect information. The information provided is solely to inform users and is not in any way a form of offer or contract unless stated otherwise.