Property-related taxes are an important aspect in every property owner’s life. However, despite the property owner’s in-depth understanding of taxes, it still remains a difficult topic to comprehend especially when it comes to Real Property Gains Tax (RPGT). However, fret not, as here’s a guide on the RPGT.

What is a Real Property Gains Tax (RPGT)

The RPGT is a form of Capital Gains Tax in Malaysia, classified into 3 tiers — individuals (citizens and permanent residents), individuals (non-citizens) and companies. This tax is levied by the Inland Revenue (LHDN) and is chargeable upon profit from the sale of your land or real property in cases where the resale price is higher than the purchase price. Ever since its first implementation in 1995, the RPGT has seen some changes in the past years — leading to its current structure. For a new owner of a property, there would be many unfamiliar terms to deal with. The Real Property Gains Tax (RPGT) and its constituents are definitely not excluded from the long list of property jargons that needs to be dealt with while investing in a future home.

A Timeline on the Changes towards the Real Property Gains Tax (RPGT)

1976

Introduction of the Real Property Gains Tax Act 1976

April 2007 – December 2009

Suspended temporarily

2010

Reintroduction of the Real Property Gains Tax

2014

The RPGT was increased for the fifth straight year since 2009

2019

Revision of the RPGT rates

2020

Another revision to the RPGT under Budget 2020, and an Exemption Order for 2020.

What is the Role of the Inland Revenue (LHDN)?

The Inland Revenue Board of Malaysia (IRBM) functions as one of the main revenue collecting agencies of the Ministry of Finance. The IRBM was established in accordance with the Inland Revenue Board of Malaysia Act 1995. This is to give it more autonomy especially in financial and personnel management. This would also improve the quality and effectiveness of the tax administration. What started off as the Department of Inland Revenue Malaysia became a board in the year 1996 and it’s now formally known as the IRBM. This agency is responsible for the overall administration of direct taxes under these acts:

Income Tax Act 1967

Petroleum (Income Tax) Act 1967

Real Property Gains Tax Act 1976

Promotion of Investments Act 1986

Stamp Act 1949

Labuan Business Activity Tax Act 1990

The Inland Revenue Board’s functions are actually quite simple. Their primary task would be to act as an agent of the Government and to provide services in administering, assessing, collecting and enforcing payment of income tax, petroleum tax, real property gains tax, estate duty, stamp duties and such other taxes, agreed between the Government and the Board. Besides that, the IRBM is also responsible for advising the Government on matters relating to taxation and liaising with the appropriate Ministries and statutory bodies on matters as such. The board acts as a collection agent for and on behalf of any body. This applies for the recovery of loans due to the act of repaying the respective bodies under any law.

The IRBM has powers as stated below:

To enter into contracts,

To utilise all property of the Board, movable and immovable, in such manner as the Board may think expedient including the raising of loans by mortgaging such property,

To engage in any activity, either alone or in conjunction with other organisations or international agencies, to promote better understanding of taxation,

To provide technical advice or assistance, including training facilities, to tax authorities of other countries,

To impose fees or charges for services rendered by the Board,

To grant loans to employees of the Board for any purpose specifically approved by the Board,

To provide recreational facilities and promote recreational activities for, and activities conducive to, the welfare of employees of the Board,

To provide training for employees of the Board and to award scholarships or otherwise pay for such training and

To do anything incidental to any of its powers.

The Aftermath of Budget 2019 towards the Real Property Gains Tax (RPGT)

During the presentation of Budget 2019, the most recent RPGT amendment was made — where Malaysians who are selling off their property in the sixth, and subsequent years of ownership will now have to pay a 5% RPGT. This was done in response to the public’s feedback on the capital gains tax, which is imposed on profit earned by homeowners and businesses by selling property. Foreigners and companies will also see an increase in RPGT rates, from 5% to 10%. In the past, homeowners in Malaysia who sold off their properties after the 5th year of ownership would not be required to pay any RPGT on the profits earned. This is in contrast with foreigners and companies who would have to pay 5% for the RPGT. This marks the 7th amendment of the RPGT to date. The shifting of the base year for the RPGT translates into lower tax payment, given the nature of appreciating property prices.

Who Should Pay the Real Property Gains Tax (RPGT)?

In the case where the selling price of a property is deemed equal to or lower than the buying price, the Real Property Gains Tax (RPGT) is inapplicable. In contrast, the RPGT should be paid if any profit exists due to the disposal of the property.

But, who should pay for the RPGT?

Well, there are 2 groups that should pay for the RPGT. Here’s a brief summary of the groups and their RPGT rate:

Individuals (Citizens, Permanent Residents, Non-citizens and Foreigners)

Regardless of their citizenship status, individual property owners are subjected to pay the RPGT. The payment is based on their chargeable gain. A chargeable gain is a profit when the disposal price is more than the purchase price of the property. For instance, if the selling price is RM 500,000 when the purchase price is RM 400,000, the house owners are subject to pay the RPGT based on the profits obtained. In this case, it’s based on the RM 100,000 profit.

Companies

Excluding companies whose core business is in real property [Real Property Companies (RPCs)]; the selling of shares by companies are not subjected to the RPGT. RPC companies are only included if they have real property or shares amounting to no less than 75% of their company’s total tangible assets. If the RPC share percentage drops below 75%, this would no longer qualify it as an RPC hence, revoking it of its RPC characteristic. The company should pay for the RPGT provision.

Costs of an RPGT

The information about the RPGT itself might be overwhelming for many property sellers. Albeit that, these property sellers should also be informed about the costs of an RPGT. It should be noted that the disposal in the 1st year means the 1st year of buying the property.

The RPGT rates from January 2019 are as follow:

wdt_ID

RPGT Rates

Individuals (Citizens and permanent residents)

Individuals (Non-citizens and foreigners)

Companies

1

Disposal in 1st year

30%

30%

30%

2

Disposal in 2nd year

30%

30%

30%

3

Disposal in 3rd year

30%

30%

30%

4

Disposal in 4th year

20%

30%

20%

5

Disposal in 5th year

15%

10%

1%

6

Disposal in 6th year and beyond

5% (2018: 0%)

10% (2018: 5%)

10% (2018: 5%)

Tax Exemptions for the RPGT

Of course, there would be exemptions towards the RPGT. However, this is only applicable in certain situations. Below are situations in which property sellers are exempted from the RPGT.

Exemption of 10% of profits or RM 10,000 per transaction

It should be noted that for citizens and permanent residents, the exemption is not applicable for transfers of an asset between siblings. However, this is indeed approved if the asset is transferred as a gift by a donor who is Malaysian and the acquirers are between husband and wife, parent and children or grandparents and grandchildren.

Besides that, there’s also the “one in a lifetime” exemption on the chargeable gain on the selling of 1 private residence by a Malaysian citizen or Permanent Resident.

For non-citizens and foreigners, if the asset is transferred between spouses, then the asset sold must be owned by the spouse who is a Malaysian. If the asset is transferred to a company, the asset owner or the spouse should be a Malaysian. In the case of joint ownership of the assets, both of them need to be Malaysians to make the transfer.

Exemption for homeowners who own low or medium cost housing priced below RM 200,000.

Exemption for companies where 10% of profits or RM 10,000 per transaction is exempted

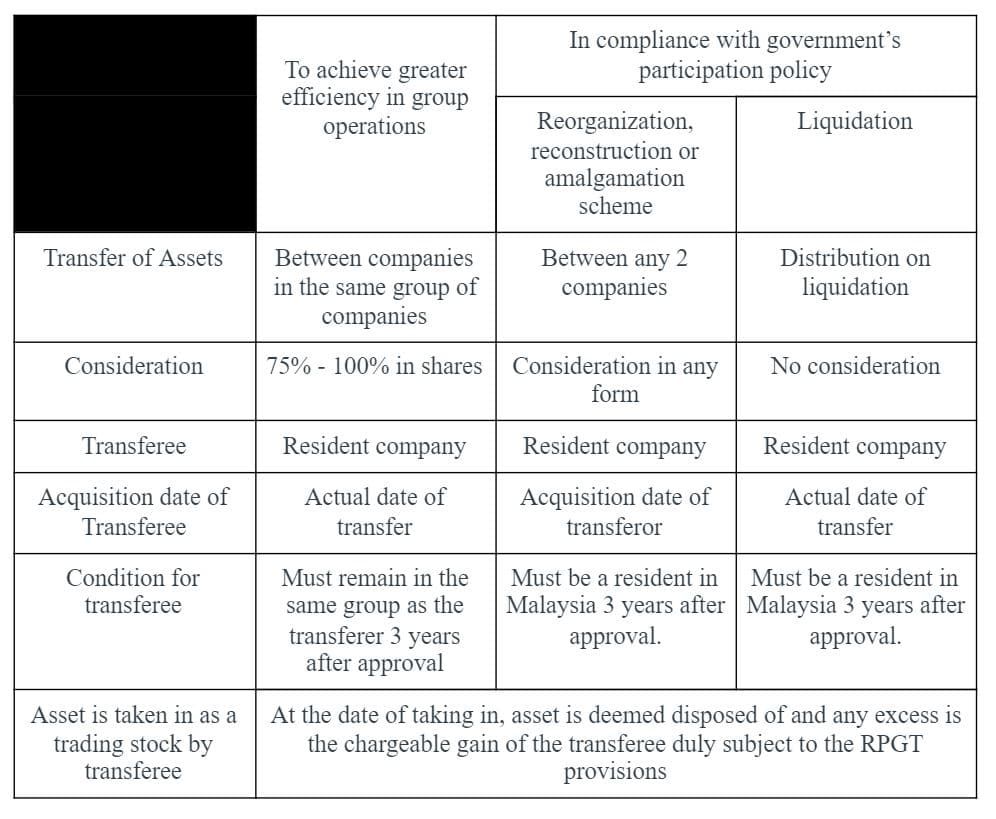

Exemption from RPGT for intercompany transfer of shares

(Shown below)

What’s a Resident Company?

If at any time, during the base year, the management and control of its affairs are exercised in Malaysia, the company is regarded as a resident company. Besides that, to be regarded as a resident company, at least one meeting of the Board of Directors should be held in Malaysia.

Allowable Loss for RPGT

Definition: An allowable loss means a loss suffered on the disposal of a chargeable asset which, if it had been a gain, would have been chargeable with RPGT.

What are the Allowable Expenses for RPGT?

Below is the list of allowable expenses for the RPGT:

Legal fees, accounting fees, surveyor’s fee

Real estate fees (sales commission)

Administrative fees

Repair or renovation to maintain or upgrade the property such as interior design such as IKEA furniture to redecorate your house

Cost of preserving or defending one’s title to, or to a right over the asset

Cost of advertising to make the disposal

Calculation of the RPGT

The method to calculate the RPGT is actually quite simple, in contrast to the confusing details regarding the RPGT.

Below are the steps to calculate the RPGT for individuals:

Net chargeable Gain: Gross Chargeable Gain – Allowable Expense – RPGT Exemption –Allowable Loss

Calculate the payable tax:

Tax Payable = RPGT Rate (based on the number of years of property ownership) x Net Chargeable Gains

An Example:

A property was purchased for RM 800,000, 5 years ago and it was sold for RM 1,000,000. The chargeable gain would be RM 200,000.

The RPGT that should be paid = RM 200,000 X 15% (determined by the number of years she’s owned the property and her citizenship status)

Hence the RPGT paid should be, RM 30,000.

Determining the applicable RPGT years

This is dependent on the date of signing the Sales and Purchase Agreement (SPA) for both completed and under-construction properties. In the case of the deceased, this is dependent on the date of the death of the individual which would be equivalent to the acquisition date by the executor.

When should the RPGT be paid?

For Malaysian citizens and permanent residents, the lawyers would retain 3% of the selling price of the property when the buyer pays the first deposit. This is for the RPGT payment. In the case of foreigners and non-citizens, the retention rate is 7%. The solicitor of the seller would make the payment to the Inland Revenue Board within sixty (60) days from the date of the sale and purchase agreement

Late RPGT Payments

After 60 days, any payment done would be subject to a penalty that should be borne by the seller. This amount is 10% of the amount of the RPGT.

FAQ

What is a Real Property Gains Tax (RPGT)?

The RPGT is a form of Capital Gains Tax in Malaysia, classified into 3 tiers — individuals (citizens and permanent residents), individuals (non-citizens) and companies.

When should the RPGT be paid?

The RPGT should be paid if any profit exists due to the disposal of the property. Individuals (Citizens, Permanent Residents, Non-citizens and Foreigners) and companies are the only 2 groups involved in the payment of the RPGT.

Will there be exemptions?

Yes, indeed. There’s an exemption of 10% of the profits for citizens if the asset is transferred as a gift by a donor who is Malaysian and the acquirers are between husband and wife, parent and children or grandparents and grandchildren. For non citizens and foreigners, if the asset is transferred between spouses, then the asset sold must be owned by the spouse who is a Malaysian.

There’s also an exemption for homeowners who own low or medium cost housing priced below RM 200,000, for companies where 10% of profits or RM 10,000 per transaction is exempted and for intercompany transfer of shares.

When should the RPGT be paid?

For Malaysian citizens and permanent residents, the lawyers would retain 3% of the selling price of the property when the buyer pays the first deposit. This is for the RPGT payment. In the case of foreigners and non-citizens, the retention rate is 7%. The solicitor of the seller would make the payment to the Inland Revenue Board within sixty (60) days from the date of the sale and purchase agreement

Will there be any penalties for late payments?

Unfortunately, yes. After 60 days, any payment done would be subject to a penalty that should be borne by the seller. This amount is 10% of the amount of the RPGT.

The information on this website is subject to change at any time without prior notice from Properly. Quantitative metrics are taken and used based on recency at the time of writing. While the Properly team takes information accuracy seriously, we are not liable for any losses due to incorrect information. The information provided is solely to inform users and is not in any way a form of offer or contract unless stated otherwise.